Price Gap Between Private & National Brands Decreases in 2021

While the number of new product introductions has fallen during the first two years of the pandemic — with private brands introducing nearly 34% fewer products in 2020 and 54% fewer products in 2021— new national CPG Brands dropped substantially more—down 46% and 65% respectively—compared to 2019.

Read More: SalesTechStar Interview With Matthew Furneaux, Lead Analyst At Loqate

Amidst the overall pullback in 2020, Private Brand retailers focused on several categories for new product growth in 2021, according to data pulled from shopper intelligence leader Catalina’s Buyer Intelligence Database.

New product introductions for retailers’ private brands have outpaced rollouts for national CPG brands during the pandemic to date, per Catalina‘s Buyer Intelligence Database.

Retailers are seeking to engage shoppers who may again be turning to private brands vs. national brands.

Tweet this

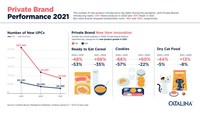

For example, the ready-to-eat cereal category saw a 48% decrease in new product introductions for Private Brands vs. a 53% decrease for national brands in 2020, the first year of the pandemic, compared to the same period in 2019. But in 2021, new product introductions for private brands increased by 66% while national brand launches declined by 35%.

Meanwhile, the cookie category experienced a 66% decline in new product introductions for Private Brands vs. a 57% decrease for national brands in 2020, compared to 2019. But in 2021, new product introductions for private brands shot up by 60% while national brands declined by 22%.

During the same timeframes, the dry cat food category experienced a 44% decline in new product introductions for Private Brands vs. a mere 5% decrease for national brands in 2020. But last year, new product introductions for private brands were up 13% while national brands declined by 8%.

Read More: EverCommerce Accelerated The Digital Transformation Of The Service Economy In 2021

Inflationary Impact On Private Brand Pricing

As consumer concern about inflation continues, private brands are reinforcing quality and value in key categories while the price differential with some national brands is shrinking, according to Phyllis Johnson, senior director of private brand development at Catalina. She points to the paper products category as an example, where bath tissue and paper towel price gaps have lessened, even as the price differential for facial tissue has remained relatively flat because of name brand price increases.

“Overall, retailers are seeking to engage shoppers who may once again be turning to private brands as they did during the early days of the pandemic when name brand shortages prompted trial,” said Johnson. “I predict this could be a second chance for those retailers to effectively demonstrate the value of private brands and convert shoppers to loyal private brand buyers.”

2021 Top Private Brand Categories

Overall, some of the private brand categories that saw the greatest growth since the COVID-19 pandemic began include: Frozen Potatoes/Baked (up 191%), Pre-Packaged Breakfast Sausage (up 173%), Disinfectant Cleaners (up 135%), Baking Ingredients (up 115%), Contraceptives (up 97%), and Home Health Testing, which includes COVID-19 kits and face masks (up 120%).